Reporting SEISS

The fifth Self-Employment Income Support Scheme (SEISS) differs from previous SEISS grants in several ways. If HMRC assesses that you are eligible self-employed for the grant they will contact you in mid-July 2021 to provide you with a personal claim date. Eligible professional individuals can apply at any time between their personal claim date and September 30, 2021.

The online claims service will be available in late July 2021.

A SEISS grant does not need repayment because it is not a loan. The SEISS are taxable in the year they are received. SEISS grants are subject to Income Tax and Class 4 National Insurance payments. As a result, the first three SEISS awards are taxable in the 2020/21 tax year and must be declared in full on your 2020/21 Self-Assessment tax return. However, in the fourth or fifth rounds if you are self-employed and your sole trader entity receives a SEISS grant, then that grant is taxable in the year 2021/2022 tax year and must be declared on your 2021/2022 Self-Assessment return.

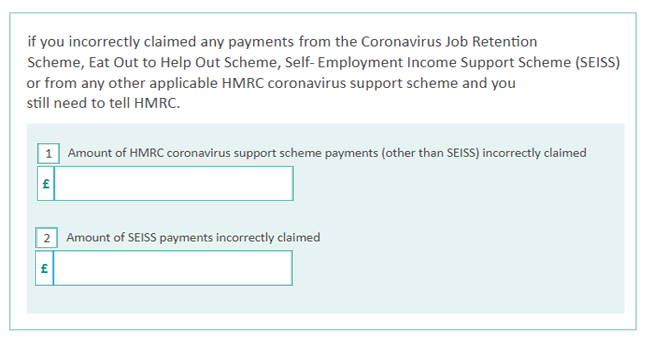

HMRC has introduced a box on the 2020/21 and 2021/22 Self Assessment tax return forms to make it easier for self-employed persons to report any money inappropriately received through SEISS awards (along with another box for CJRS).

Any deviation in the SEISS grants should be disclosed on SA tax returns, according to ICAEW TAX guide 12/21. The revenue and customs have stated that it will provide a remedy for autocorrect returns in early July, although it may take longer to sort the backlog of previously submitted returns. These adjustments are proper if the grants were not reported on the return; however, they are inappropriate if the grants were recorded on the return but in the incorrect box.

In this case, the taxpayer or their agent must make an amendment; rejecting HMRC's rectification will not address the problem. If you received a SEISS grant that you were not entitled to or were paid more than you should have, you must inform HMRC within 90 days and agree to repay the money, otherwise, you may face a penalty. If you received a SEISS grant that you were not entitled to or were paid more than you should have, you must inform HMRC within 90 days and agree to repay the money, otherwise, you may face a penalty.

According to HMRC, sole businesses will not be required to register for VAT if the money they get from SEISS exceeds the VAT threshold (currently £85,000 per year). For VAT purposes, SEISS is not part of your taxable turnover. If the effects of the coronavirus (COVID-19) have rendered you unable to pay your self-assessment tax bill, you may be able to pay in more manageable monthly installments. “This includes any delayed (deferred) ‘payments on account' that were due in July 2020, if you did not pay them at the time,” according to Gov.UK. For further information, go to Gov.UK.